The February Nationwide HPI has shown that annual house price growth has slipped into negative territory for the first time since June 2020, and is the weakest level since November 2012

According to the February Nationwide HPI, there was a 0.5% month-on-month fall, with prices 3.7% lower than in August 2022.

In February, the average house price was £257,406, dropping from £258,297 in January. London house prices remain considerably higher, remaining £250,000 above the UK national average.

House prices drop for the sixth month in a row

Commenting on the February Nationwide HPI, Nationwide chief economist Robert Gardner said: “Annual house price growth slipped into negative territory for the first time since June 2020, with prices down 1.1% in February compared with the same month last year. Moreover, February saw a further monthly price fall (-0.5%) – the sixth in a row – which leaves prices 3.7% below their August peak (after taking account of seasonal effects).

“The recent run of weak house price data began with the financial market turbulence in response to the mini-Budget at the end of September last year. While financial market conditions normalised some time ago, housing market activity has remained subdued.

‘A result of the financial pressures that have been weighing on households for some time’

Gardner continued: “This likely reflects the lingering impact on confidence as well as the cumulative impact of the financial pressures that have been weighing on households for some time. Indeed, inflation has continued to outpace wage growth and mortgage rates remain significantly higher than the lows recorded in 2021.

“Even though consumer sentiment has improved in recent months, it is still languishing at levels prevailing during the depths of the financial crisis.”

Mortgage rates are not in line with house prices

“It will be hard for the market to regain much momentum in the near term since economic headwinds look set to remain relatively strong, with the labour market widely expected to weaken as the economy shrinks in the quarters ahead, while mortgage rates remain well above the lows prevailing in 2021.

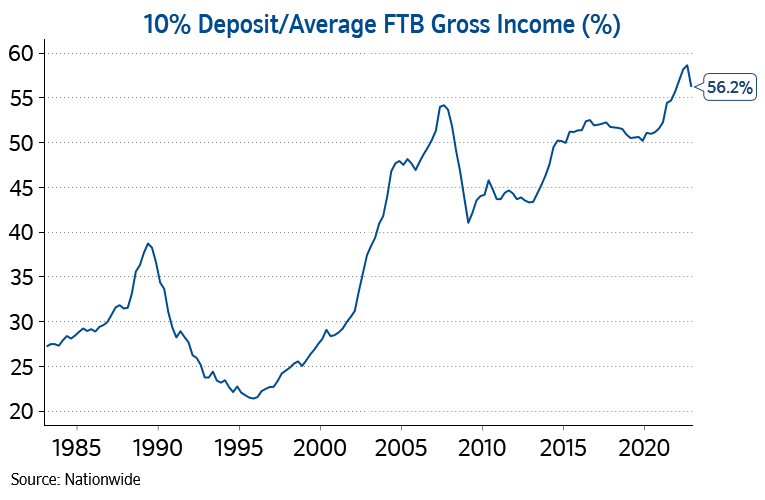

“Indeed, despite the modest fall in house prices, for a prospective first-time buyer earning the average income looking to buy the typical home, mortgage payments remain well above the long run average as a share of take-home pay.

“In addition, deposit requirements remain prohibitively high for many and saving for a deposit remains a struggle given the rising cost of living, especially for those in the private rented sector, where rents have been rising strongly.”

Demand for new homes continues to far outpace supply

Ben Woolman, director at Woolbro Group, added: “Britain’s property market is descending into a standoff in which spooked sellers are jumping the gun.

“Those who are being low-balled with paltry offers falling far below asking prices should instead hold their nerve and wait until buyer borrowing power returns, which it inevitably will.

“Despite the doom and gloom, it is looking increasingly likely that inflation could fall below 2% by the end of the year. If that prediction comes to pass, then it will give us a much clearer picture of when the Bank of England might start to lower the base rate, resulting in lower mortgage costs — albethey not as low as they were before the cost of living crisis.

“Still, this could very well be the trigger point at which a greater number of buyers begin to ramp up their househunting efforts once again, injecting more competition into the market and driving up offers on properties.

“Moreover, despite demand for new homes continuing to far outpace supply, Britain’s antiquated planning system means we are still nowhere near to building the required number of new homes each year. Consequently, this will continue to prop up prices.”