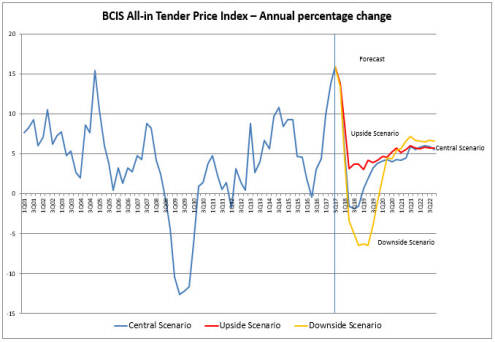

Tender prices rose sharply in the first half of 2017, but are expected to fall over the year to Q4 2018. This is against a background of new work output remaining static in 2018, and uncertainty about the effect of Brexit negotiations in the private commercial sector

The current BCIS forecasts are based on the UK’s exit from the EU at the end of the two-year period following the signing of Article 50, followed by a ‘transitional period’ of two years.

The Office for National Statistics (ONS) report that total new work output rose by 5.5% in 2017. In the BCIS ‘Central’ forecast, new work output is expected to remain almost unchanged in 2018, with a sharp fall in private commercial work being balanced by increases in the remaining new work sectors. Despite a further sharp fall in private commercial output, modest growth in total new work output is forecast for 2019. Stronger growth returns in the final three years of the forecast period, driven by strong growth in infrastructure output, and a return to growth in the private commercial sector.

Materials costs rose quite strongly in 2017, driven in part by the fall in Sterling exchange rates. Materials prices are expected to rise by 3% to 4% per annum over the forecast period.

BCIS is now assuming that there will be restrictions on the movement of labour following a two-year transitional period. This will impinge on the construction industry from around Q1 2021, as the supply of new European labour dries up. This will put upward pressure on promulgated wage awards as the unions try to keep pace with higher site rates obtained due to the reduced labour pool. Site rates over and above promulgated rates will be reflected in the market conditions factor, putting upward pressure on tender prices.

Wage awards are expected to be settled at around an annual 3% over the first three years of the forecast period, then 5% in 2021 and in 2022.

With total new work output expected to remain unchanged in 2018, tender prices are expected to fall by 1.6% in the year to Q4 2018. With only modest output growth in 2019, tender prices are expected to recover slowly over the first half of 2019, but rise by an annual 3.8% by Q4 2019, albeit the increase is exaggerated by the fall in tender prices a year earlier. With output gaining strength over the final three years of the forecast period, and with strengthening cost pressures, tender prices are expected to rise by around 4% to 6% per annum over the remainder of the forecast period. Upward pressure on site rates will also put upward pressure on tender prices over the final year of the forecast period.

Central forecast

Over the forecast period (4Q17 to 4Q22):

- New work construction output will rise by 15%;

- Input cost of resources will rise 20%; and

- Tender prices will rise 19%.

BCIS has produced two further scenario forecasts based on different assumptions on the Brexit agreement and their impacts on construction demand (see graph).