Rebecca Larkin, head of Construction Research at the Construction Products Association (CPA) explores the challenges and future of the construction economy amidst a turbulent economic climate

It seems as though I’ve used the phrase ‘interesting times’ for a long time now. It sums up the constant uncertainty, deteriorating confidence and low visibility that have accompanied the EU Referendum, Brexit itself, the coronavirus pandemic, Russia’s invasion of Ukraine and most recently, a period of historically high inflation.

It has obviously been an unprecedented and volatile few years for the economy during and post-pandemic, and it seems strange that even with today’s levels of uncertainty, it registers as a position of relative stability.

Nevertheless, it’s a stability that is characterised by low quarterly rates of GDP growth that have been hovering around zero since the beginning of 2022, and the economy is yet to return to its pre-pandemic size.

Although at only 0.2% below where it was in the fourth quarter of 2019, it hasn’t got far to go. This current weakness has inevitably raised the spectre of recession, but it has been inflation reaching its highest rate for 40 years that has dominated the headlines over the period.

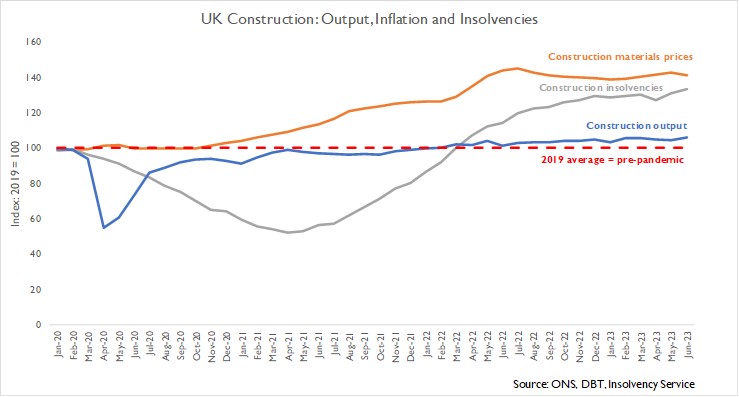

Consumer and industrial input prices spiked rapidly following the Russia-Ukraine war

Consumer and industrial input prices were first driven higher by rising demand after lockdowns were eased and then spiked rapidly in 2022 following the Russian invasion of Ukraine.

This resulted in sharp increases in global oil and commodity prices that then filtered into wider price inflation through higher costs for fuel, energy, transport and raw materials.

The Bank of England has chosen to focus on reining in inflation rather than stimulating growth, which is not surprising as its primary remit is to maintain price stability, as defined by the government’s target of CPI inflation of 2% – plus or minus 1 percentage point.

Monetary tightening has taken interest rates up from the record-low of 0.1% in December 2021 to 5.25% currently. They were last at this level in early 2008, before the global financial crisis and when UK GDP growth was much stronger, averaging 0.7% per quarter.

With inflation still well above this target, and even more stubbornness in core inflation, which excludes food, alcohol, energy and tobacco, market expectations are for a peak in interest rates close to 6% at the end of the year and perhaps remaining at this level longer than previously expected.

Despite a turbulent economy, construction output has displayed stronger overall performance

Encouragingly, over the last couple of years, the construction economy has displayed a stronger performance than the overall economy, even at a time of hefty rates of input cost inflation, particularly for materials.

In the second quarter of 2023, construction output was 5.6% above the pre-pandemic levels of 2019, against a backdrop of materials and component costs being 43.2% higher and wages 14.8% higher.

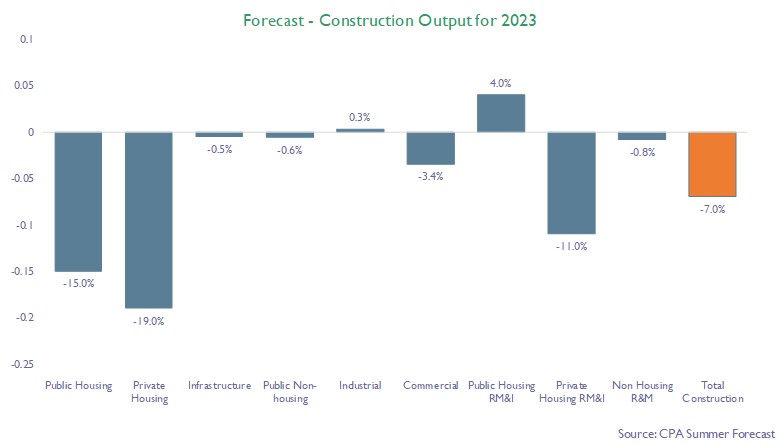

So after outperforming GDP since 2020, is the strength in the construction economy likely to continue? Unfortunately, is appears to be a ‘no’.

A lack of momentum in the economy is leading to weaker construction demand

Things have shifted noticeably throughout 2023 already and notably so in three of the sectors that have driven previous growth: private new build housing, industrial and infrastructure.

It appears that we’ve now reached the point after two years of strong inflation eroding consumer and business spending power, steep increases in interest rates and the recent, albeit small, uptick in the unemployment rate, where the lack of momentum in the economy is translating into weaker construction demand.

The start of the Bank of England’s tightening cycle had an instant effect on homebuyer demand – clearly evidenced in the sharp declines in reservations and order books, as well as slower build rates reported in house builders’ market updates.

Furthermore, with lingering uncertainty over when we reach the peak in interest rate rises and how higher mortgage rates and general living costs play out on demand over the next 6-12 months, private new housing, which accounts for just under a quarter of construction economy output, is now grappling with a sharp contraction.

The industrial construction sector is on the decline

Support for first-time buyers, who are most reliant on mortgage lending, is a potential offering from the government. This seems more likely as a sweetener as we approach a general election year, but would still need potential buyers to balance this with the overall strain on finances and raising a deposit.

Industrial construction – primarily factories and warehouses – has been the star performer in terms of output growth since 2020, reflecting investment decisions made immediately post-pandemic to increase manufacturing capacity (factories) and the increases in demand for associated storage but also facilities linked to e-commerce (warehouses) which is part of a longer-running structural trend.

However, as with housing, confidence to proceed with new factories investment has been hamstrung by the stagnant economic backdrop. In fact, recent manufacturer announcements that existing facilities are now surplus to requirements point to a large gap in the pipeline of upcoming new build projects.

New capital tax allowances for business investment are unlikely to override weak sentiment. For warehouses in particular, the investment cycle is expected to have peaked, especially for speculative builds, for which developers were accustomed to ultra-low interest rates for finance. Borrowing costs three or four times higher now make these investments much less attractive.

Large multi-year projects like HS2 are at risk of being paused as financial constraints continue

In infrastructure, growth is typically driven by large multi-year projects, but these are also the most at risk of being paused, delayed or cancelled as government priorities change.

The two-year delays announced to upcoming projects like HS2 phase 2a (Birmingham to Crewe), the Lower Thames Crossing, the A27 and the Port of Liverpool Access road are cases in point that limit future growth, whilst the reassessment of HS2 work at Euston removes a considerable volume of activity from the current pipeline.

Financially-constrained local authorities add another downward element, with numerous examples of multi-million-pound cost increases putting the brakes on infrastructure schemes.

Just as consumer price inflation has begun decelerating, recent data from the Department for Business and Trade has shown a sharp moderation in price inflation for construction materials since April, so whilst it will be less of an issue, it is important to point out that a roll back to the price levels seen back in 2019 or 2020 is improbable.

The key consideration is how badly these past years have already bruised the supply chain. Insolvencies within construction have risen 32% in the 12 months to June and were 51% higher than in 2019.

If we consider that this has been during a time when construction activity remained high, then the prospect of work becoming more scarce as activity declines presents a clear risk over the next 12 months.

The ‘interesting times’ look set to continue rolling on.

Rebecca Larkin

Head of Construction Research

Construction Products Association (CPA)

www.constructionproducts.org.uk